Built at the Intersection of Machine Learning, Financial Regulation, and Indian Credit Scale

Why this problem. Why now. Why infrastructure — not a product.

Between 2022 and 2024, Indian NBFCs and digital lenders deployed ML-based credit scoring at a pace that outran the governance infrastructure available to support it. The RBI's Digital Lending Guidelines of September 2022 required lenders to communicate the grounds of rejection to applicants and to maintain model risk management frameworks adequate to the complexity of the models in use. The FREE-AI (Framework for Responsible and Ethical Enablement of AI, RBI) principles, articulated through successive guidance notes, demanded explainability, fairness, and human oversight as operational properties of AI systems in regulated lending. What lenders actually had, in most cases, was a score, a binary decision, and no documented pathway between the two. Millions of credit decisions were being made each year by models that were, from a regulatory standpoint, functionally opaque — not because the technology for explainability did not exist, but because no one had built the layer of infrastructure that would make explainability native to the decisioning workflow rather than a retrospective exercise conducted under audit pressure.

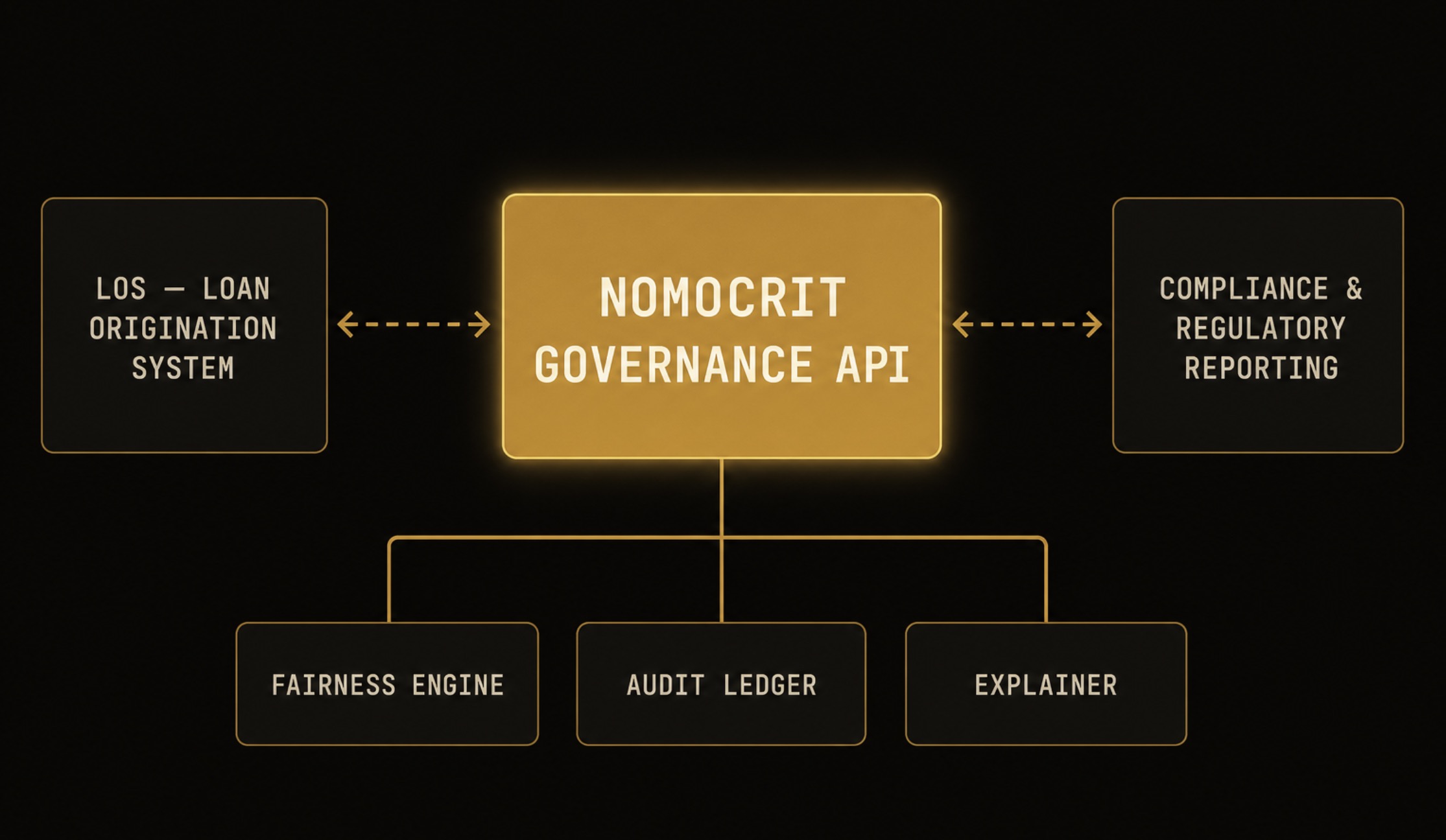

NomoCrit was built on a specific architectural conviction: that governance cannot be added to an AI system after the fact. When explainability is a report generated by a separate team in response to a complaint, it is not explainability — it is documentation theatre. When fairness is a quarterly dashboard reviewed by a compliance officer with no mechanism to act on what it shows, it is not fairness monitoring — it is observation without enforcement. The founding insight was that the problem facing Indian lenders in 2023 was not a missing feature in their credit models. It was a missing layer in their technology stack — the layer that sits between the model's output and the regulatory surface, and that makes every property the regulator cares about a first-class output of the decisioning process rather than an annotation applied afterward. NomoCrit is that layer.

Responsible AI in lending has become a category of marketing claim in Indian fintech. Lenders describe their models as transparent, their processes as fair, their outcomes as explainable — and mean, in most cases, that they have a policy document that says these things. NomoCrit's position is more precise: responsibility for a credit decision is not a posture; it is a property of the infrastructure that produced the decision. A lender cannot be accountable for a decision they cannot reconstruct. A regulator cannot audit a model that produces no decision artifact. For NomoCrit, “accountable” has a specific operational definition: every credit decision generates a structured artifact containing the decision basis, the feature contributions, the threshold applied, and the recourse pathway available to the applicant. Every artifact is stored in a form that supports audit. Every audit is completeable — from the examiner's first request to a complete decision ledger — within 72 hours. Accountability is not a value; it is a latency specification.

The regulatory environment for AI in Indian lending is consolidating in a way that has no recent precedent. The FREE-AI framework establishes expectations for model governance that are sector-specific and operationally detailed. The Digital Personal Data Protection Act of 2023 introduces data principal rights — including the right to information about automated decisions — that will require lenders to produce decision explanations as a matter of legal obligation, not voluntary practice. The Digital Lending Guidelines of 2022 are mature enough that RBI supervision of compliance is becoming substantive rather than procedural. The window between “we have deployed AI” and “we can demonstrate that our AI is governed” is narrowing. Lenders who build on accountable infrastructure now — who instrument their decisioning stack to produce the required artifacts as a natural output of the process — will not face the reconstruction problem when enforcement timelines arrive. Those who wait will find that retrofitting governance onto an existing model deployment is significantly more expensive, and significantly less reliable, than building it in from the start.

The outcome NomoCrit is building toward is one in which the question “why was this applicant rejected?” has a complete, consistent, and legally defensible answer at every point in the credit cycle — not because someone worked backward from the model to reconstruct a justification, but because the answer was generated the moment the decision was made. The applicant who is rejected understands precisely which factors in their financial profile drove the outcome, and can access a documented pathway to contest or improve their position. The regulator who audits a lender's AI operations finds a complete decision ledger, structured for review, with fairness metrics and threshold governance logs intact. The model that begins to drift against a shifting credit population is detected before it produces a cycle of discriminatory outcomes. This is not a product vision. It is a description of what Indian lending infrastructure looks like when it is built correctly — and it is the outcome toward which every design decision in NomoCrit is oriented.

The governance API layer in the Indian lending stack.

Advait Karnatak

Building the governance infrastructure that Indian lending systems need to operate transparently under the RBI’s FREE-AI Framework. NomoCrit is the decision layer between model inference and regulatory accountability: built for scale, designed for audit.

[ CONNECT ]Explainability is not a feature. It is the contract.

Every AI decision that cannot explain itself is a liability — regulatory, legal, and ethical. NomoCrit is built on the premise that explainability must be present at the decision point, at decision latency, for every decision. Not available on request. Not reconstructed for auditors. Present.

Governance infrastructure outlasts any single model.

Models will be retrained, replaced, and upgraded. The governance infrastructure that records, explains, and audits their decisions must outlast all of them. NomoCrit is not built around a model — it is built around the decision record.

Regulatory alignment is a floor, not a ceiling.

Compliance with the RBI FREE-AI principles and the DPDP Act is the minimum bar NomoCrit meets — not the aspiration. The aspiration is lending infrastructure that is accountable because it is designed to be, not because it is regulated to be.